Introduction

Any conversation about the progression of technology, especially cryptocurrency dominance to new developments in cybersecurity, appears to revolve around the word “blockchain.” Although blockchain technology has countless uses, many people need to become more familiar with it.

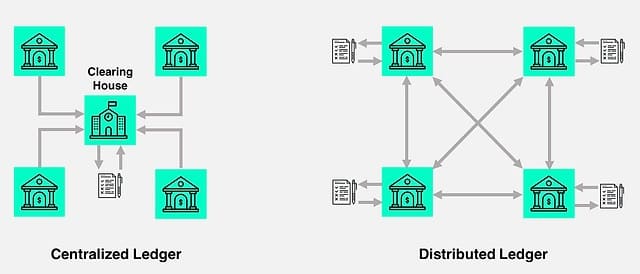

In the past, financial transactions were kept in financial institutions and recorded in written ledgers. Auditing of traditional ledgers was possible, but only for individuals with special access. Blockchain democratized these ideas by removing the confidentiality surrounding handling information, particularly transaction data.

What is blockchain?

A blockchain is, at its most basic level, a decentralized list of transactions that is regularly updated and scrutinized. It is also referred to as distributed ledger technology (DLT) and may be configured to track and record anything of significance across a network spanning several places and businesses. As a result, a vast spider web of connected computers forms.

In simpler way, a blockchain technology is a technology to create a backend utilize to store data. Each data set is stored in a block, hence all the data are stored in multiple blocks connected with each other in logical form. Additionally, these data are stored in distributed manner in different servers spread across the world. Thus, this technology enhances the security of the data significantly and is gaining popularity rapidly.

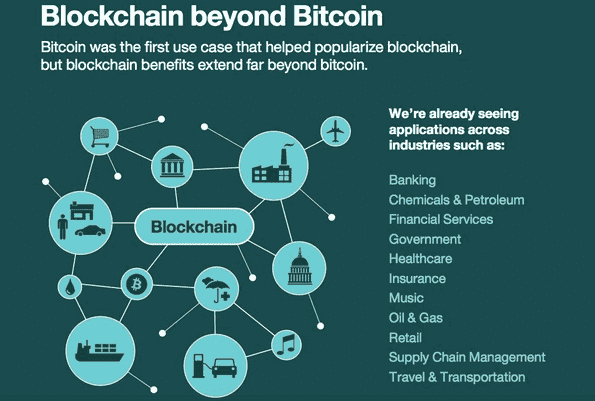

Although blockchain technology is commonly linked to cryptocurrencies, it’s not just applicable to digital asset markets. It has a unique capacity for adding and storing data, enabling it to carry out various additional tasks across numerous industries.

How does a blockchain appear?

The block and the chain are the components that make up a blockchain.

A block is a group of data chronologically connected to other blocks in a virtual chain. Imagine a blockchain as a railway with several connected carriages, each carrying a specific quantity of data. Blocks can only accept a given amount of information before getting full, much like the commuters in a train carriage.

Each block has a timestamp, which shows the day and time the data was captured and saved. Timestamps are crucial for supply chain or transaction data since they show when a transaction or package was handled, which is significant information.

How many ledgers are there in total?

There is no central server copy of a blockchain. Instead, each computer user that adds to the network, or “node,” maintains their copy of the ledger and regularly verifies it with the other nodes to guarantee that everyone shares the same data record. No single failure point exists since each contributor maintains their copy. It is also hard for hostile actors to alter the data recorded on blockchains because of this excellent protection layer.

If a hacker organization wanted to alter any transactions on a blockchain, they would need to invade the computers of every single network participant around the globe and alter all records to reflect the same information.

The blockchain is open and transparent, aspires to be decentralized, distributed over networks, and, in several situations, fully public, unlike a conventional institution’s repository of financial records. The blockchain can serve as a single point of truth by emphasizing transaction and data storage openness.

In what way does data uploaded to a blockchain?

Blockchain is a secure way to store data and be transparent with it. The following illustrates how a transaction is inserted into a new block in the context of “Bitcoin”:

A message containing the public addresses of the sender, receiver, and the amount being sent is generated whenever a bitcoin client submits a transaction. The sender hashes the data after adding their private key to it (turns it into a fixed-length code.) It creates a digital signature that attests to the sender’s intention to send the recipient of bitcoin.

Before broadcasting it to the network, the sender bundles this digital signature with the message and their public key. It is comparable to saying, “Hello, everybody! I want to transfer this person some bitcoin.”

(Note: For most wallets and other programs, this happens “under the hood” without requiring user interaction.)

The bundled transaction is added to a “mempool” of other pending transactions that have not yet been confirmed before being put into the blockchain.

A batch of transactions from the mempool is taken by Bitcoin network miners who have successfully found new blocks using proof-of-work (usually based on which ones have the highest fees attached). Verify each transaction to make sure the senders have the right amount of bitcoin in their wallets, process it through software to make sure the packaged data (digital signatures, messages, and public keys) are valid, add it to the new block, and then broadcast the proposed new block to the network so that other miners can verify everything is accurate.

Similar to the way proof-of-stake blockchains operate, but with individuals known as “stakers” or “validators” finding and confirming transactions instead of mining nodes.

Nodes have a wide range of capabilities. In the case of validator nodes or mining nodes, these include maintaining a historical record of all transaction data, validating transactions, and adding new blocks to the blockchain. Once a transaction has been added and authorized, the information cannot be revised or modified. Data kept on a blockchain network is therefore referred to as “immutable.” Similar to the way proof-of-stake blockchains operate, but with individuals known as “stakers” or “validators” finding and confirming transactions instead of mining nodes.

Additional uses for blockchain technology

The blockchain does away with the necessity for intermediaries like banks. Peer-to-peer networks cut out the intermediary and enable safe transactions that anybody can examine.

Using blockchain technology is for more than just financial transactions. Hospitals are using blockchain technology to track patient data and increase accuracy. Agricultural businesses utilize it logistically to follow the food distribution chain. Smart contracts make use of it to record all commitments and state changes. It has lately evolved into a means of authenticating, trading and selling original digital artwork.

Blockchain technology is more prominent in how we work, live, and interface with digital data. As with any new, groundbreaking technology, there isn’t a single set of norms, and the implications are still uncovered. However, it is undeniably here to stay.